Q4 2025 Earnings Call Transcript")

")

A person is showered with money.

In investing, it can be easy to fall into the trap of buying what everyone else is buying. This is just basic human psychology. However, it can be detrimental to your investing results.

That is because when you are buying hot stocks, you’re also often paying excessive valuations that come with greater downside when the underlying companies disappoint and sentiment inevitably sours. This is one of the biggest reasons why, on average, retail investors tend to dramatically underperform the stock market over the long haul.

I would argue the opportunity to make real money lies in buying high-quality, high-yielding dividend stocks while they are out of favor. That is because boring and unappreciated stocks can be obtained at dirt-cheap valuations. Low valuations are accompanied by easy expectations to surpass. Eventually, market sentiment inverts, and such stocks revert to their fair value. In the meantime, investors benefit from dividend payments.

Enbridge (NYSE:ENB) is a stock that is one of the more convincing buys in the market today. Let’s dig into the company’s fundamentals and valuation to understand why I am initiating a strong buy rating.

DK Research Terminal

Even with 10-year U.S. treasury bonds yielding 4.8%, Enbridge’s 8.2% dividend yield is exceptionally attractive. The good news is that this mouth-watering starting income is also secure: Enbridge’s DCF payout ratio of 65% is significantly below the 83% payout ratio that rating agencies view as safe for the midstream industry.

Beyond its viable payout ratio, the company also has a healthy balance sheet going for it. Enbridge’s debt-to-capital ratio of 0.5 is moderately less than the 0.6 that rating agencies want to see from midstream industry companies. This helps to explain how the company earns an investment-grade BBB+ credit rating from S&P on a stable outlook. Put into perspective, Enbridge is at just a 5% risk of closing its doors between now and 2053. For these reasons, Dividend Kings awards the company a perfect 5/5 dividend and balance sheet safety rating.

As if Enbridge’s exceptional quality wasn’t convincing enough, the valuation is a downright steal at the current $31 share price (as of October 27, 2023). Relative to a fair value estimate of $46 a share, the stock is priced at a staggering 31% discount to fair value.

Here’s what Enbridge’s total return profile could look like over the next 10 years:

- 8.2% yield + 5% FactSet Research annual growth forecast + 3.8% annual valuation multiple expansion = 17% annual total returns or a 381% total return versus the 10% annual total returns or a 160% total return for the S&P 500 index (SP500)

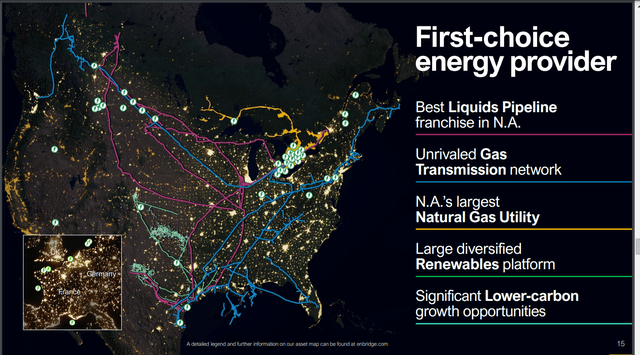

North America’s Leading Midstream Company

Enbridge Investor Day 2023 Presentation

Stretching throughout much of continental North America, Enbridge’s energy infrastructure is extensive. The company’s pipelines transport approximately 30% of the crude oil produced in North America and around 20% of the natural gas consumed in the United States. Put another way, the world couldn’t live without Enbridge’s crude oil and natural gas pipelines.

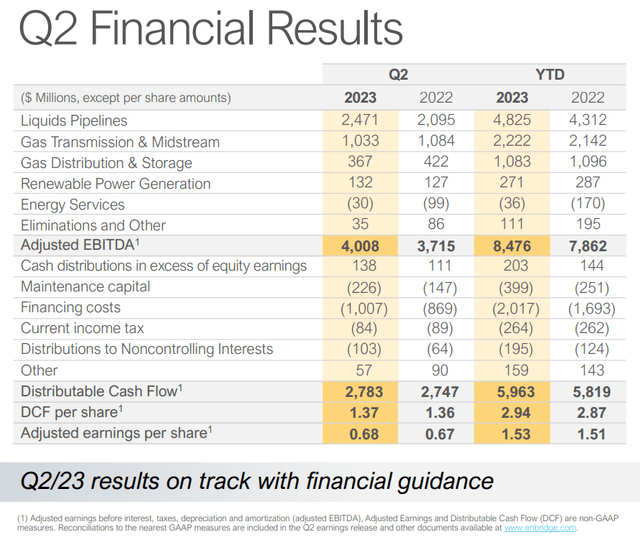

The necessity of the company’s energy infrastructure to the modern economy explains its solid operating results so far in 2023. Enbridge transported a record 3.1 million barrels a day of product on its mainline system through the first half of the year (slide 5 of 18 of Enbridge Q2 2023 Investor Presentation). For context, this was up about 200,000 barrels a day over the year-ago period.

Enbridge Q2 2023 Investor Presentation

This is what propelled the company’s adjusted EBITDA 7.8% higher over the year-ago period to $8.5 billion CAD in H1 2023. Higher financing costs due to surging interest rates weighed on Enbridge’s results. That is why the midstream company’s DCF per share grew at a slower rate of 2.4% year-over-year to $2.94 (in CAD) during the first half.

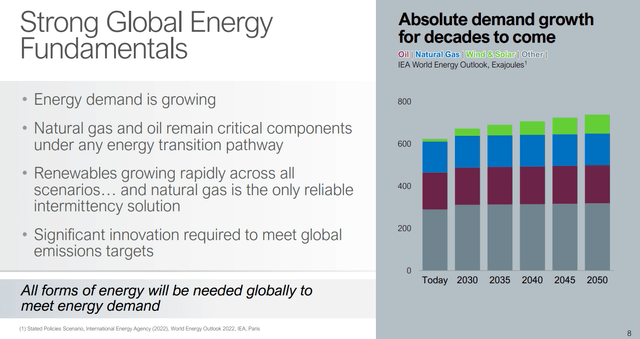

Enbridge Investor Day 2023 Presentation

Looking toward the future, total global energy demand is expected to steadily rise in correlation with economic growth and population growth between now and 2050. All forms of energy are going to be needed to support this rising energy demand, which should lead to higher volumes moving through Enbridge’s infrastructure in the years to come. That is why FactSet Research pegs the company’s annual growth consensus at 5% for the long run.

Though not as much of a financial fortress as Enterprise Products Partners (EPD), Enbridge’s balance sheet isn’t shabby, either. As fellow SA analyst Fluidsdoc recently noted, the acquisition of Dominion Energy’s (D) natural gas utilities for $14 billion (including debt) will add some near-term strain to the balance sheet. However, the deal will nearly double Enbridge’s pro-forma utility revenue to just shy of 25%, making the company’s cash flows more predictable. That is likely why the outlook for the company’s BBB+ credit rating from S&P remains stable.

Enbridge Has Dividend Growth Left In The Tank

Having upped its dividend for 28 consecutive years, Enbridge’s dividend growth streak is impressive. The company’s dividend growth isn’t going to be massive moving forward. But when you’re starting with an 8%+ dividend yield, growth doesn’t have to be very high.

Enbridge has paid $1.775 in dividends per share (in CAD) for the first half of 2023. Against the $2.94 in DCF per share (in CAD) generated during that time, this equates to a 60.4% payout ratio. That’s on the very low end of its targeted payout ratio range of between 60% and 70% of DCF. This is why I expect annual dividend growth ranging from 3% to 5% annually in the years ahead from Enbridge.

Risks To Consider

Enbridge is a world-class business. Yet, the company faces its share of risks to consider before buying.

First off, Enbridge is a Canadian company. In taxable brokerage accounts, there is a 15% Canadian withholding tax for United States-based investors. Fortunately, owning the stock in retirement accounts can shield investors from the withholding tax. That could save the headache of having to file for a tax credit on taxable account dividends.

In the long term, Enbridge faces the risk of not appropriately adapting its business model to the energy transition ahead. The good news is that with the company incorporating carbon capture storage, hydrogen, and renewable natural gas into the mix, the probability is very high that the company will be fine.

Finally, Enbridge’s infrastructure is a valuable target for hackers. That is why it is of utmost importance that the company continue to do everything that it can to stave off a cyber breach. If Enbridge were to be successfully hacked on a major scale, its operations could be materially impacted.

Summary: Enbridge Has Big Income, Modest And Sustainable Growth, And Huge Valuation Upside

Zen Research Terminal

Top to bottom, Enbridge is a well-run business. The company is steadily growing, the balance sheet is respectable, and DCF easily supports the dividend. Not to mention that among its industry peers, Enbridge is in the 96th percentile of managing its risks.

The market’s mistake could be your buying opportunity with this 13/13 ultra SWAN per Dividend Kings’ quality rating system. This is because Enbridge is trading 31% below its fair value estimate of $46 right now. If the market came to its senses in the next 12 months, the stock could deliver total returns approaching 50%.

In the more likely scenario, it will take a while before Enbridge returns to its rightful value. Still, the annual total return potential for the stock is superb, all the while shareholders can collect a safe and massive dividend.

- 8.2% yield + 5% annual growth + 3.8% annual valuation multiple upside = 17% annual total returns versus 10% annual total returns for the S&P 500

Read the full article here

Q4 2025 Earnings Call Transcript")

")

")